按 Enter 到主內容區

:::

回首頁

兒童網頁

網站導覽

意見信箱

雙語詞彙

常見問答

English

關鍵字查詢:

進階查詢

熱門 :

人民幣

匯率

利率

外匯存底

開放資料

您的瀏覽器不支援JavaScript語法,JavaScript語法並不影響內容的陳述。您可使用按鍵盤上的Ctrl鍵+ (+)鍵放大/(-)鍵縮小來改變字型大小;回到上一頁可使用瀏覽器提供的 Alt+左方向鍵(←) 快速鍵功能;列印可使用瀏覽器提供的(Ctrl+P)功能。您的瀏覽器,不支援script語法,若您的瀏覽器無法支援請點選此超連結

Sitemap

最新消息

最新消息

新聞稿

即時新聞澄清

貨幣政策與支付系統

貨幣政策簡介

貨幣政策最終目標

貨幣政策架構及相關考量

貨幣政策制定及執行

貨幣政策工具及政策傳遞管道

貨幣政策溝通策略

向立法院業務及專題報告

重要支付系統概述

中央銀行同業資金調撥清算作業系統

票據交換結算系統

跨行金融資訊系統

中央銀行中央登錄債券清算交割系統

貨幣政策工具

準備金制度

貼現窗口制度

公開市場操作

公開市場操作相關統計資料

公開市場操作制度

公開市埸操作相關法規

小規模附買回測試操作

金融機構轉存款

選擇性信用管理

理監事會議決議

利率及準備率

利率

央行貼放利率

前日金融機構牌告存放款利率異動資訊

「五大銀行平均存款利率」與「五大銀行平均基準利率」

金融機構牌告利率資訊查詢專區

五大銀行存放款利率歷史月資料

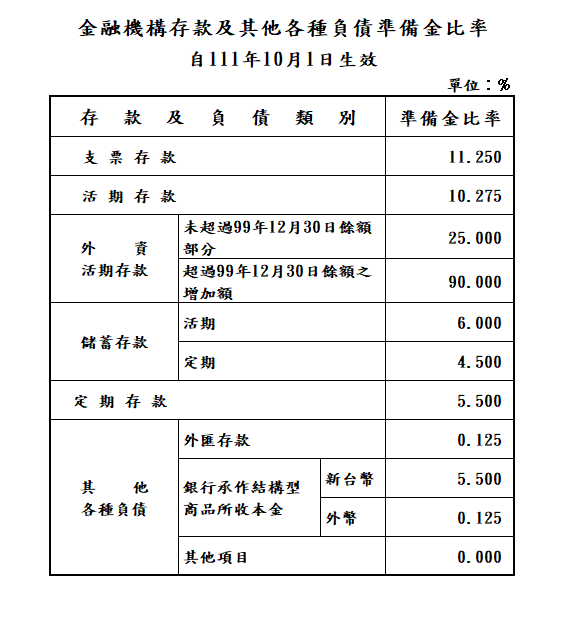

準備率

存款及其他各種負債準備金比率

銀行存放央行準備金乙戶利率

準備金調整申報作業

發行貨幣

發行貨幣專區

統計資料

每日通貨發行數

每季新臺幣發行數額及準備狀況

破獲偽造新臺幣案件之獎金核發原則

偽造鈔券案件

偽造硬幣案件

相關規定事項

新臺幣短片及防偽

中央印製廠

中央造幣廠

外匯資訊

外匯法規

外匯通函彙編

新臺幣對美元銀行間成交之收盤匯率

兩岸貨幣清算

兩岸貨幣清算通函

兩岸貨幣清算新聞稿

兩岸貨幣清算機制簡介

出進口外匯收支統計

出進口外匯收支統計

地區性金融統計填表資訊

外幣結算平台

國際金融業務分行(OBU)概況

中央銀行新臺幣兌美元換匯交易餘額及外幣拆款餘額

國際準備與外幣流動性

國庫收支與政府債券

國庫收支

中央政府債券

統計與出版品

統計

統計資料庫

預告統計資料發布時間表(連結至行政院主計總處網頁)

重要統計事項變更預告專區

我國與主要貿易對手通貨對美元之匯率

金融統計

重要金融指標

金融機構放款與投資及金融市場票債券發行餘額/變動數

證券劃撥存款

消費者貸款及建築貸款餘額

五大銀行(台銀、合庫銀、土銀、華銀及一銀)新承做放款金額與利率

存放款加權平均利率

金融統計月報(IMF格式)

金融統計月報

本國銀行營運績效季報

銀行衍生性金融商品交易量統計

銀行衍生性金融商品名目本金餘額統計

金融健全指標

國際收支與國際投資部位

國際收支

國際投資部位

資金流量統計

公民營企業資金狀況調查

資金流量統計

中央銀行財務報表

中央銀行資產負債簡表

中央銀行損益簡表

統計編報手冊

公務統計報表程式

出版品

主題服務

央行辦理健全房地產市場方案專區

作業規定

問與答

全文檔案

購置住宅貸款

購地貸款

餘屋貸款

工業區閒置土地抵押貸款

其他

本行相關新聞稿

相關網站連結

辦理情形

焦點金融議題與常見問題

央行主管法令規章(含訴願決定)

法令規章及訴願決定查詢系統

法規英譯徵集意見專區

法規命令草案年度立法計畫專區

金融穩定與監理

金融穩定

金融穩定-簡介

總體審慎措施

各國金融穩定報告網站連結

金融健全指標

中華民國金融穩定報告

金融穩定相關研究報告

金融監理資訊

中央銀行金融檢查制度

報表申報作業

本國銀行營運績效季報

金融法規查詢

全國金融機構一覽

主動公開政府資訊

請願之處理結果及訴願之決定

組織與職掌

施政計畫及執行情形

經營政策

內部控制聲明書

向立法院業務及專題報告

業務統計

利率及準備率

外匯資訊

金融穩定與監理

支付系統運作

經理國庫

發行貨幣

金融、國際收支、資金流量統計等

出版品

辦理人民申請提供政府資訊案件統計

國家賠償案件統計

研究報告

委託研究報告

公務出國報告

預算及決算資料

預算

決算

會計報表

書面之公共工程及採購契約

會費、補(捐)助、媒體政策及業務宣導等

委託調查及會費捐助

對民間團體及個人補(捐)助

媒體政策及業務宣導

中央銀行理監事聯席會議決議

與民眾有關宣導事項

流通鈔券真偽之辨識

舊版新臺幣券兌換

郵政儲金機動利率

愛惜鈔券

穩定物價

個人資料保護

中央銀行保有個人資料檔案公開項目彙整表

遊說法資訊專區

公股股權管理

行動應用軟體服務績效

經濟金融動態

資料開放

消費者資訊

性別平等專區

中央銀行性別平等推動計畫及成果報告

中央銀行性別平等專案小組

性別統計專區

性別統計指標

中央銀行所屬委員會性別比例達成情形

相關網站連結

性別分析報告

性別意識培力

CEDAW專區

性騷擾防治專區

其他相關連結

財團法人資訊公開專區

財團法人名冊及相關規範

財團法人基本資料

預決算資料

查核資料

其他資料

連結網站

認識央行

央行簡介

現任首長

歷任首長

組織與職掌

理監事名單

現任一級主管

職員進用方式

首長演講辭

中央銀行法

兒童網頁

:::

最新消息

2025-07-03

114年7月364天期定期存單開標結果

2025-07-02

有關某不動產業者反映本行信用管制措施導致民眾無法申辦地上權貸款,特此說明

2025-06-30

本行受財政部委託訂於114年7月11日標售5年期114年度甲類第8期中央政府建設...

2025-06-30

114年5月全體金融機構流動準備計提情形

2025-06-30

114年5月銀行衍生性金融商品交易量統計

更多

新聞稿

2025-07-03

114年7月364天期定期存單開標結果

2025-07-02

有關某不動產業者反映本行信用管制措施導致民眾無法申辦地上權貸款,特此說明

2025-06-30

114年5月全體金融機構流動準備計提情形

2025-06-30

114年5月銀行衍生性金融商品交易量統計

2025-06-27

中央銀行重要人事異動

更多

即時新聞澄清

2024-11-28

網路社群流傳誤導民眾有關本行信用管制方向之影片,特此公告澄清

2023-11-01

本行單位主管名義遭詐騙集團冒用行騙,特此公告澄清

2022-06-01

有關本行第16期金融穩定報告提及我國政府財政狀況之說明

2019-10-07

有關媒體報導本行政策利率動向之說明

2019-06-05

有關外媒關注臺灣壽險業投資美國債券市場之說明

更多

公開市場操作

2025-07-03

114年7月3日中央銀行公開市場操作資訊

2025-07-03

114年7月364天期定期存單開標結果

2025-07-03

114年7月3日中央銀行存單申購發行資訊

2025-07-02

114年7月2日中央銀行公開市場操作資訊

2025-07-02

114年7月2日中央銀行存單申購發行資訊

更多

電子布告欄

2025-06-30

本行受財政部委託訂於114年7月11日標售5年期114年度甲類第8期中央政府建設...

2025-06-23

財政部114年度第3季債券發行明細表

2025-06-23

發售「2024年第三屆世界12強棒球錦標賽冠軍紀念銀幣」公告

2025-06-17

114年金融控股公司資金狀況調查

2025-06-16

114年證券公司資金狀況調查實施說明

更多

徵才公告

2025-06-10

建築專業人員(辦事員)

2025-05-19

經濟金融研究專業人員(助理研究員同等級)

更多

影音專區

2024年第三屆世界12強棒球錦標賽冠軍紀念銀幣記者會114.6.23

更多

重要指標

新臺幣/美元銀行間收盤匯率

2025-07-02

29.019

新臺幣/美元銀行間收盤匯率

更多

外匯存底

2025.05(十億美元)

592.95

外匯存底

更多

貨幣總計數M2年增率

2025-06-19

3.33%

貨幣總計數M2年增率

更多

金融業隔夜拆款利率

2025-07-02

0.823%

金融業隔夜拆款利率

更多

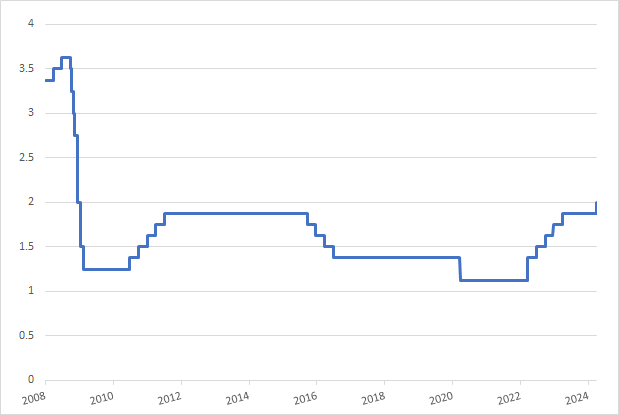

重貼現率

2024-03-22

2%

重貼現率

更多

準備率

2024-10-01

(請點選)

準備率

更多

重大政策

114年6月19日央行理監事會後記者會簡報及外界關心之議題

114年6月19日央行理監事會後記者會參考資料

中央銀行理監事聯席會議決議新聞稿

更多

服務專區

推薦服務

中央銀行因應氣候變遷策略方案

中央銀行對金融機構辦理不動產抵押貸款業務規定修正規定

不動產貸款相關資訊

向立法院業務及專題報告

公開市場操作

更多

熱門服務

新臺幣/美元 銀行間收盤匯率

央行辦理健全房地產市場方案專區

利率

金融統計

本行發行存單

更多

便民服務

中央銀行提供政府資訊申請書

中央銀行檔案應用申請

中央銀行人民申請案件處理時限表

中央銀行人民陳情案件處理時限表

中央銀行兩公約教育訓練教材

更多

出版報告

中央銀行季刊第47卷第1期(114年1月)

中央銀行季刊第46卷第4期(113年12月)

中央銀行季刊第46卷第3期(113年9月)

中央銀行季刊第46卷第2期(113年6月)

中央銀行季刊第46卷第1期(113年3月)

更多

相關連結

主題網站

性別平等專區

資料開放

貨幣金融知識專區

社群媒體專區

券幣數位博物館

央行主管法令規章

金融機構一覽

統計資料庫

更多

相關政府及金融機構

中央印製廠

中央造幣廠

財政部國庫署

行政院主計總處--統計調查受訪者專區

全國法規資料庫入口網站

更多

國際組織

Asian Development Bank (ADB)

Asia-Pacific Economic Cooperation (APEC)

Bank for International Settlements (BIS)

Central American Bank for Economic Integration (CABEI)

European Bank for Reconstruction and Development (EBRD)

Financial Stability Forum

更多

我國之支付系統運作機構

財金資訊公司

台灣期貨交易所

中華民國証券櫃台買賣中心

台灣票據交換所

聯合信用卡處理中心

更多

展開

OPEN

最新消息

最新消息

新聞稿

即時新聞澄清

貨幣政策與支付系統

貨幣政策簡介

向立法院業務及專題報告

重要支付系統概述

貨幣政策工具

理監事會議決議

利率及準備率

發行貨幣

發行貨幣專區

統計資料

破獲偽造新臺幣案件之獎金核發原則

相關規定事項

新臺幣短片及防偽

中央印製廠

中央造幣廠

外匯資訊

外匯法規

外匯通函彙編

新臺幣對美元銀行間成交之收盤匯率

兩岸貨幣清算

出進口外匯收支統計

地區性金融統計填表資訊

外幣結算平台

國際金融業務分行(OBU)概況

中央銀行新臺幣兌美元換匯交易餘額及外幣拆款餘額

國際準備與外幣流動性

國庫收支與政府債券

國庫收支

中央政府債券

統計與出版品

統計

出版品

主題服務

央行辦理健全房地產市場方案專區

焦點金融議題與常見問題

央行主管法令規章(含訴願決定)

法規命令草案年度立法計畫專區

金融穩定與監理

主動公開政府資訊

資料開放

消費者資訊

性別平等專區

財團法人資訊公開專區

認識央行

央行簡介

現任首長

歷任首長

組織與職掌

理監事名單

現任一級主管

職員進用方式

首長演講辭

中央銀行法

兒童網頁

Facebook

Youtube

Instagram

中央銀行APP

意見信箱

訂閱電子報

收合/CLOSE

回頁首